As expected, much of the weakness in Canada in Q3 was with the external side of the economy with exports slipping by 5% (reflecting weak US demand) and imports rising 6.4% (reflecting strong Canadian demand for foreign goods). The overstretched housing sector in Canada also contributed to the Q3 slowdown as residential construction fell by 5.3% in Q3.

But outside of residential construction, domestic conditions in the Canadian economy have remained solid, with consumer spending up 3.5% ( the gain was widespread across spending categories suggesting that the consumer remains confident.) Perhaps the most encouraging development was that the Canadian business sector reawakened in the the third quarter with business investment in machinery and equipment up by a whopping 29%. This likely reflects the impact of a high Canadian dollar, which makes the costs of imported capital equipment from the US cheaper.

Implications

With economic growth downshifting to a below trend rate after blistering ahead through the initial stages of the recovery, Canada is joining the"modest economic growth club" (aka the rest of the developed world.) For 2010 as whole, growth looks like it will come in at roughly 3% in Canada which should only slightly outpace the 2.8% growth rate expected in the US. In 2011, growth in Canada and the US is projected to be 2.4% and 2.3% respectively, again not terribly different in terms of the aggregate picture, with both countries growing below their potential. Given the slower pace of Canadian growth, I think its a good bet that the Bank of Canada will hold off on resuming any rate hikes until the second half of 2011.

Some Perspective

Despite the subpar headline GDP number , its important to keep in mind that the major source of the slowdown in the Canadian economy is due to external factors. In particular, weak exports to the US and higher imports act as a considerable drag on a small open economy like Canada. In contrast, the domestic side of the economy has continued to perform well, particularly compared to the US, whose domestic economy continues to cope with deleveraging and severely bruised banking sector:

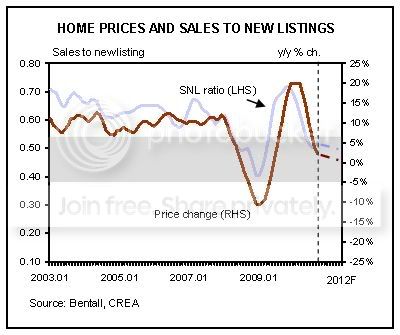

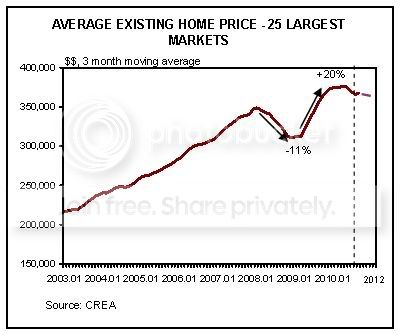

Going forward, it looks like the Canadian economy will have to continue relying on domestic demand to support overall growth given the weakness in the rest of the world. This is a major reason why the Bank of Canada will be forced to keep interest rates low, as this will provide some necessary cushion to keep supporting domestic spending. Of course, domestic demand will still cool down from its current outsized levels, if only because of exhausted demand in the previously booming housing market. But let's be clear about one thing - Canada's stable mortgage market and banking system should prevent this housing slowdown from evolving into a US-style "capitulation" that would have secondary "knock off" effects in the rest of the economy.